The liberalization of the European electricity sector (The same liberatization model can been found in other countries), promoted by Directive 96/92/EC of the European Parliament, has meant that the large electricity companies, which have traditionally represented a series of roles such as generators, transporters, distributors and retailers, have split into a conglomerate of different companies, each with a very specific role.

In most cases, this separation of roles has been determined by an incompatibility of activities established by the aforementioned directive or by the particular application of the directive in the form of a law in the different states that comprise the European Union. Thus, for example, the generation and transmission or distribution of electricity are incompatible activities and therefore a company that owns energy generating units cannot own/operate electricity transmission or distribution networks.

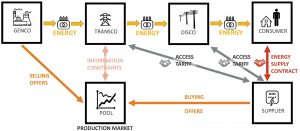

Fig. 1 Simplified scheme of the electrical sector actors’ interactions

In the diagram of the Fig. 1 we can see a simplified scheme of the different agents that exist in the electrical system. As we can observe, traditionally, and assuming that there is no distributed generation in the distribution network, the energy is injected into the transmission grid by the generating companies (GENCOs), this energy flows through the transmission grid (owned by a so called TRASCO or also TSO) at a high voltage to reduce losses and the voltage is reduced once the final consumption is approached. This voltage reduction is done through step down substations that connect the high voltage transmission grid to the medium voltage distribution grid owned by a distribution company (DISCO or DSO). There are end-users which obtain energy from the medium voltage distribution grid (or even from the transmission grid), but the vast majority of domestic users obtain energy from the low voltage distribution grid that is connected to the medium voltage grid through small distribution transformer stations.

In relation to the interactions between agents and the roles of each one, we can see in the diagram how the retailer establishes energy contracts with the consumer, the establishment of this type of contract is totally liberalized allowing the provision of different services ranging from conventional ones with an energy term, to the so-called flat rates in which the consumer basically pays a fix fee and can consume “unlimited” energy with the only restriction of not exceeding a certain power. Another more sophisticated type of tariff includes so-called implicit demand response programmes in which the retailer sends the consumer a price signal either the day before or in real time so that the consumer adjusts his consumption to those price signals.

To acquire energy, the retailer buys it from the electricity pool by submitting bids for purchasing energy. The electricity pool is operated by the market operator which is responsible for matching the offers to buy energy submitted by the retailers with offers to sell energy submitted by the generators. Generation and retailing are not compatible because the strategies for submitting bids to the pool of these two agents are opposed, while the retailers pursue the purchase of energy at the lowest possible price, the generators aim to obtain the highest price. The activity of buying and selling energy is also a liberalized activity as the agents who make bids for the purchase and sale of energy at the pool are free to select the bid prices and energy packages always within limits pre-established by the regulator.

Once the retailer has acquired the energy packages, it needs to transport that energy to the final consumer following the energy flow described above, for which it must pay an access fee to the transporters and also to the distributors for the use of their networks. In the majority of European countries transport and distribution operate as geographical monopolies, i.e. once a company has its network deployed within a certain geographical area, another company cannot deploy a second redundant network. In return, in these cases, the regulator classifies both transmission and distribution as regulated activities (as opposed to all other liberalized activities), and thus sets the prices that third party agents have to pay to distribution and transmission network owners for the use of their networks. In a very simplified way, we could say that the generators receive incomes from the sale of electricity in the pool, and the transporters and distributors receive regulated incomes from the payment of the access tariff but also from the investments they make in keeping their networks in optimal conditions. The retailer on the other hand receives its revenues from the supply contracts established with consumers and its main expenses are the payment of the access tariffs to distributors and transporters and the payment for the energy obtained through the pool. There is also a modality in which retailers and generators establish bilateral contracts bypassing the pool matching mechanism (an example of this would be the Power Purchase Agreements or PPAs ).

The procedure described above applies to several types of markets, but especially to the so-called day-ahead market where generators and retailers negotiate the energy packages to be sold/bought on each of the 24 slots (each of them representing an hour) of the following day. It must be pointed out that once the daily market is closed and all purchase and sale bids are matched, the market operator (MO, represented in Fig 1 as the pool) check with the transmission system operator (TSO whether or not the transmission grid is capable of handling the power flows resulting from the energy transactions. If technical constraints related to the overload of transmission system elements and voltage levels are not met, the TSO activate a set of correction mechanisms that will modify the matching performed by the MO and that they are explained later on in this document.

In the previous paragraphs and in the Fig. 1 diagram, for the sake of simplicity, it has been assumed that both retailers and generators operate individually in the market. However, in doing so, they are responsible for the possible power imbalances. In other words, generators are responsible for generating the energy they have sold and retailers for delivering the energy they have bought.

Designing the best strategy to operate in the market as well as taking responsibility for the energy balance in each of the so-called imbalance settlement periods (ISPs) is a very complex and specialized task. A bad strategy when designing purchase and sale offers can lead to being left out of the equation. On the other hand, once a certain bid is closed, maintaining the committed balance during each of the 24 hours is also complicated.

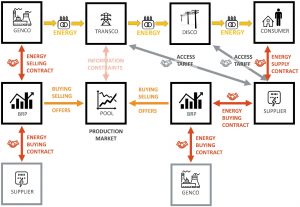

For this reason, both generators and retailers usually close agreements with specialized trading companies which will design the optimized operation strategies for their customers (which in this case will be generation units, retailers or other consumption units). We will refer to this type of companies as Balance Responsible Parties (BRPs). It must be taken into account that although generation and retailing are not compatible activities, a generator and a retailer are allowed to contract the services of the same BRP, and this is normally the case. A BRP usually has in its portfolio both retailers and generators with different technologies, since the joint management of a wide and varied portfolio of clients allows to compensate certain imbalances with other ones, thus reducing their risk of imbalances and the cost directly generated by them (penalties). BRPs and their role are represented in Fig. 2. In this representation a more realistic representation of how the different agents interact in the production market is provided.

Fig. 2 Production market representation considering BRPs

The above-mentioned day-ahead market is a so-called production market. The mission of the production markets is to close the energy transactions between actors that will carry out the energy exchange within a time horizon that is at least a few hours away from the closing of the market. The production markets are usually operated by the market operator (MO, represented in the figure as the “pool”) and, in addition to the day-ahead market, there are a number of intraday markets in all European countries. There are two types of intraday markets, conventional (intraday auction markets) and a continuous intraday market also called (single intraday coupling).

Regarding conventional intraday markets, they usually last one hour and their application window is separated by a few hours from the closing. For example, in the case of the Iberian electricity market affecting Spain and Portugal, the first intraday market extends from 14:00 to 15:00 hours and it handles energy transactions from midnight on the same day (day D) to midnight the following day (day D+1). The rest of the intraday markets are staggered in time, opening at 5pm, 9pm, 1am, 4am and 9am. They last approximately one hour and they handle energy transactions that can be made from approximately 3 hours after closing time until midnight on day D+1. Fig. 3 shows the structure and application periods of the different markets.

In the case of the continuous intra-day market, the difference with the conventional market is that the rounds are continuous and agents from all European areas can participate as long as maximum power is not reached at the international interconnection points. Furthermore, energy transactions can be agreed only one hour in advance.

It is very important to note that in the day-ahead market, the generators or their respective BRPs represent the role of energy sellers while the retailers or their respective market representatives (BRPs) play the role of buyers. This does not have to be the case in the different intraday markets. Suppose for example that a generator has sold in the day-ahead market on day D, 10MWh for the hourly period from 14:00 to 15:00 on day D+1. However, at 23:00 hours on day D the generator detects a fault in one of its groups and determines that for the period under study it will only be able to produce 8MWh. The generator could wait for the opening of the next intraday market (Intraday number 5 opening at 1 a.m. of day D+1) and buy the remaining 2MWh to maintain the balance. It could be the case that these 2MWh are sold by a retailer which has bought them on the day-ahead market but has determined that it will not be able to deliver them.

In the previous paragraphs, we have explained how the purchase and sale of energy is carried out in the day-ahead market and how corrections are established in the successive intraday markets. As it has been seen, there are correction mechanisms in the different production markets which allow to correct unforeseen imbalances at the time of the closing of the intraday market but foreseen in the successive hours.

However, obviously, the sum of the electrical power demanded plus the system losses has to be equal to the generation at all times. Keeping the energy balance in the Imbalance Settlement Periods is not enough for the stability of the system. When an imbalance occurs, the frequency of the system is affected in such a way that if generation exceeds demand plus losses, the frequency will increase. The frequency will decrease if demand plus losses exceeds generation.

The transmission system operator TSO has a set of market mechanisms which allow it to maintain this balance at all times through by monitoring the frequency and the so-called balance service providers (BSP). These market mechanisms are grouped into what are called operation markets. The difference between production and operation markets is that in the case of operation markets, they are managed by the system operator (TSO) and not by the market operator (MO). In addition, production markets are energy markets because what is traded are energy packages, while operating markets are hybrid markets. They are hybrid markets because they energy markets but also capacity markets where in some cases certain actors are remunerated for the capacity to produce or vary their generation/consumption. In general, we could say that BRPs participate in the production markets while BSPs participate in operating markets. In the general case BRPs and BSPs may be different agents (as for example the case of Belgium), in that case the transactions of balance services made by a certain BSP would affect one or more BRPs. It is very common for the role of BSP to be assumed by a BRP-type company as these roles are not separate in many European countries.

Fig. 3 Scheme containing the different kind of electrical markets

The balancing services that a BSP or in its absence a BRP can provide to the TSO are varied and will be described below.

On the one hand, there is the primary regulation also called frequency containment reserves (FCR), which is a decentralized frequency control service that is mandatory for all generators capable of providing it. Traditionally, this type of generators used to be large generators with a very high inertia, but nowadays any load or generator that can act quickly when faced with a change in frequency could provide the primary regulation. The power variation that an element makes in the event of activating the primary regulation does not need to be maintained in time beyond a few seconds. In the case of prosumers, if they could act very quickly in the event of frequency variations, they could be providers of primary regulation. The remuneration for primary regulation capacity varies from one country to another, while in countries such as Spain it is a compulsory but nonremunerated service. In countries such as Belgium, the Netherlands or Germany primary regulation capacity is auctioned weekly.

In addition to primary regulation, secondary and tertiary regulations are also balance services. In the case of secondary regulation, this is a power-frequency control service that is handled centrally and with market mechanisms, as opposed to primary regulation, which acts automatically in a decentralized manner. In other words, generators that modify their power in the case of primary regulation do so because they are programmed to operate without receiving any external order or having a central control that coordinates them. This is due to the need for very rapid action in the case of primary regulation. However, in the case of secondary regulation, the required power variation to adjust the system frequency is done a few seconds after the frequency fluctuation has occurred. The power variation provided by secondary regulation then replaces the primary regulation and is dispatched automatically but in a centralized way, that is why it is also called automatic Frequency Restoration Reserves (aFRR).

The secondary regulation rising or decreasing power must be maintained during an imbalance settlement period (ISP), traditionally 15 minutes. It has traditionally been a compulsory but remunerated service for generation units that could provide it but the service could also be provided by prosumers or demand units. In this service, the availability to increase or decrease power is remunerated, as well as the extra energy that is injected or no longer injected into the system if the secondary regulation is activated. In countries like Spain, this service is auctioned the day D affecting the day D+1 as it can be observed in the Fig. 3. The cost of this service is transferred to the demand and generation units that generated the imbalance or to the BRPs that represent such agents.

Tertiary regulation is similar to secondary regulation but it acts after an imbalance settlement period has passed to release secondary regulation and can extend several ISTs, 2hours in the case of countries such as Spain. Tertiary regulation services are also called manual Frequency Reserve Restoration. Normally, those units that subscribe to this service are obliged to offer an up or down regulation band.